SBA Update — PPP Loans: Applications for new Paycheck Protection Program (PPP) loans are now closed. If you are ready to apply for forgiveness of your PPP loan, see below for important information and read our Loan Forgiveness Checkup.

SBA Update — PPP Loans: Applications for new Paycheck Protection Program (PPP) loans are now closed. If you are ready to apply for forgiveness of your PPP loan, see below for important information and read our Loan Forgiveness Checkup.

Learn about the PPP, how you should prepare for the Loan Forgiveness phase, and what reports you will need from ADP.

The Paycheck Protection Program (PPP) offered forgivable low-interest loans to small businesses facing uncertainty due to COVID-19, to help businesses retain workers, maintain payroll, and cover other existing overhead costs.

Loan Forgiveness Details & Reports

Up to 100 percent of the PPP loan is forgivable (to the extent that employers meet certain requirements, such as maintaining employment and wage levels). The loan will be fully forgiven if:

In addition, the COVID-19 relief law passed by Congress in December 2020 provides that the forgiven portion of a PPP loan can be excluded from gross income. Borrowers have 10 months from the end of their covered period to apply for forgiveness before they would need to start paying back any portion of their loan. Lenders have 60 days to make a decision on loan forgiveness.

The new round of PPP funding includes other important changes to the PPP loan forgiveness process, some of which may apply to loans issued previously in 2020. ADP is actively evaluating these changes and will update the guidance below and in the PPP Loan Forgiveness Reports as additional guidance is issued by the Treasury Department and Small Business Administration. For example, the CAA 2021 provides that the SBA will issue a streamlined forgiveness application form for loans of $150,000 or less. This one-page form would require borrowers to certify certain information related to loan forgiveness, list the amount of the loan, number of employees retained and estimated amount of the loan spent on payroll costs. Borrowers would be required to retain – but not submit – documents substantiated their forgiveness application for 4 years for employment records and 3 years for other records.

For borrowers who are interested in applying for forgiveness now, the Treasury Department and SBA previously issued a Loan Forgiveness Application Form, an “EZ” version of the Loan Forgiveness Application, and instructions for each, all of which are available here. Additionally, borrowers who previously received loans of $50,000 or less may be exempt from reductions in loan forgiveness amounts based on reductions of full-time equivalent employees or in salaries or wages. If eligible, borrowers would use the SBA Form 3508S, or their lender’s equivalent form, to submit their loan forgiveness application. ADP has put together a Loan Forgiveness Checkup which outlines important steps to take before year-end to maximize loan forgiveness.

Here are some frequently asked questions about loan forgiveness. Guidance on loan forgiveness is evolving and rules may change, so check back for updates.

Yes, the amount of the loan can be fully forgiven as long as certain conditions are met. The specific amount will generally depend in part on what portion of the loan is used on eligible payroll costs and whether the employer has maintained staffing and pay levels during the covered period.

A loan may be fully forgiven if all the following three conditions are met:

To obtain full forgiveness, loan proceeds must be spent within the 8- to 24-week period immediately following disbursement of the loan. If you pay your employees on a biweekly or more frequent schedule, you may choose to begin the covered period on the first day of the first pay period following disbursement of the loan (“Alternative Payroll Covered Period”) for qualifying payroll costs only.

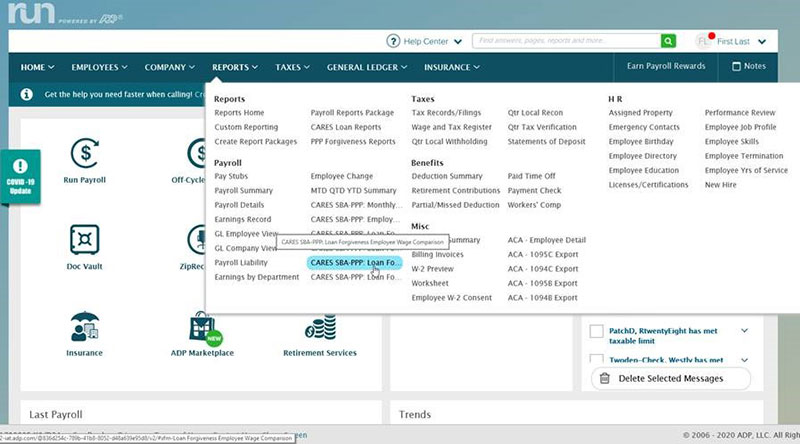

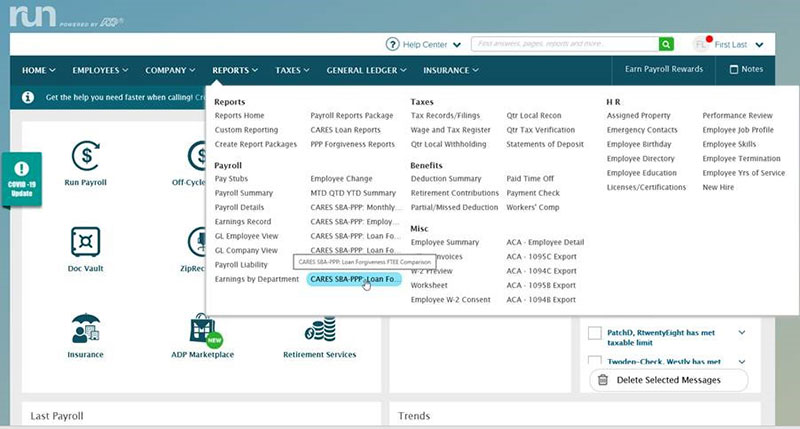

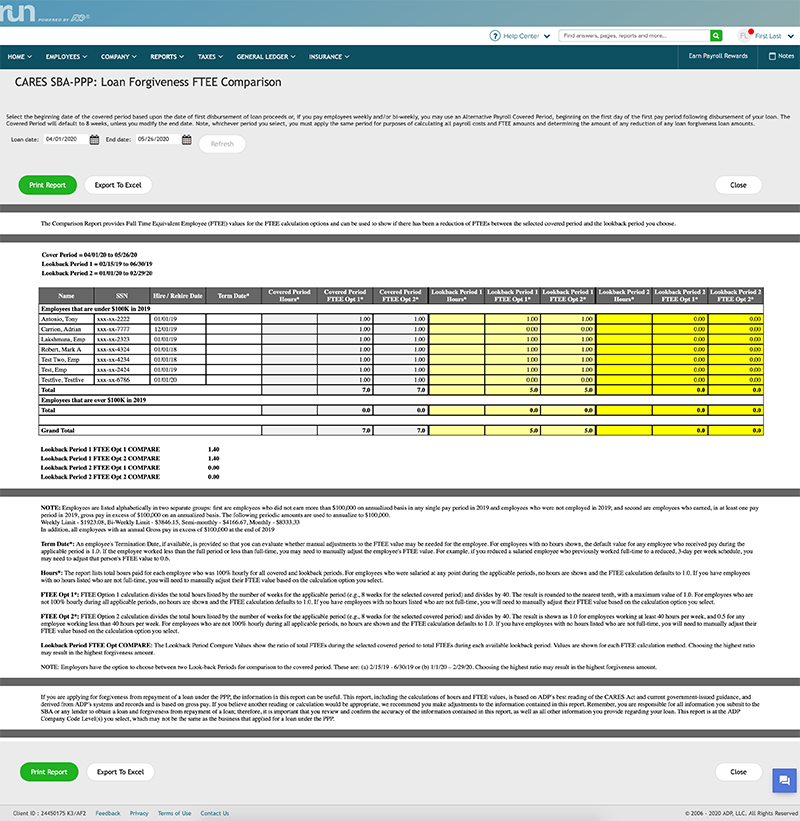

To determine whether staffing levels have been maintained, the average number of full-time equivalent employees (FTEEs) during the applicable Covered Period or Alternative Payroll Covered Period will be compared to one of two time periods. Borrowers may either use the period from February 15 through June 30, 2019 or January 1 through February 29, 2020. For instance, if the employer had 20 FTEEs from February 15 through June 30, 2019 and 18 FTEEs from January through February 2020, the borrower would most likely choose the latter time period since it may be more advantageous to use the lower FTEE number for the chose lookback period. If the number of FTEEs during the Covered Period or Alternative Payroll Covered Period is lower than the time period chosen, the amount of loan forgiveness may be reduced proportionately.

Seasonal employers may compare the average FTEEs employed during the Covered Period or Alternative Payroll Covered Period to either period listed above or to any consecutive twelve-week period between May 1 through September 15, 2019.

Note that your forgiveness amount will not be reduced by a failure to maintain staffing levels during the Covered Period or Alternative Payroll Covered Period if (a) your average FTEEs between February 15 and April 26, 2020 is lower than your FTEES as of February 15, 2020, and (b) you restored the level of FTEEs on or before the end of the applicable Safe Harbor period to be equal or higher to the FTEE levels as of February 15, 2020. The Safe Harbor period ends on December 31, 2020 for borrowers who received their PPP loan prior to August 8, 2020, and on the last day of the chosen covered period for borrowers who received their PPP loan or Second Draw PPP loan in or after December 2020. There are other exceptions that may apply. See the question below discussing rehiring employees.

Repayment of part of the loan may be required if an employee’s average annual salary (for salaried employees) or average hourly rate (for hourly employees) are reduced by 25% or more during the applicable Covered Period or Alternative Payroll Covered Period compared to the period of January 1 though March 31, 2020 (for borrowers in the first PPP round).

However, if (a) a given employee’s wage levels (annual salary level for salaried employees and hourly wages for hourly employees) between February 15 and April 26, 2020, are lower than as of February 15 and (b) you restore the wage levels by the end of the applicable Safe Harbor period to be same or higher than as of February 15, 2020, there will be no reduction in forgiveness based on that employee’s wage levels. The Safe Harbor period ends on December 31, 2020 for borrowers who received their PPP loan prior to August 8, 2020, and on the last day of the chosen covered period for borrowers who received their PPP loan or Second Draw PPP loan in or after December 2020.

Note: When comparing wage levels to determine if your loan forgiveness amount will be reduced, employees who earned wages or a salary at an annualized rate of more than $100,000 in any pay period of 2019 aren’t considered.

Loan forgiveness will not be reduced based on an inability to rehire employees if the employer can document (1) written offers to rehire individuals who were employees of the organization on February 15, 2020; or (2) an inability to hire similarly qualified employees for unfilled positions by the end of the safe harbor period.

Additionally, forgiveness will not be reduced for failure to maintain employment levels if the organization is able to document an inability to return to the same level of business activity as existed prior to February 15, 2020, due to compliance with COVID-19-related guidance for sanitation, social distancing, or worker or customer safety requirements from the Health and Human Services (HHS), the Centers for Disease Control and Prevention (CDC), or the Occupational Safety and Health Administration (OSHA).

The SBA has suggested that the documentation required above would be satisfied if an employer made a good faith, written offer of rehire at the same salary/wages and for the same number of hours, the employee rejected the offer of rehire, and the employer notified the applicable state unemployment insurance office of the employee’s rejection of rehire within 30 days. Employees who are terminated for cause, voluntarily resign, or voluntarily request and receive a reduction of hours may also be excluded from the FTEE reduction calculations.

Under the PPP, payroll costs generally include:

Note: The definition of payroll costs excludes employer federal taxes, workers compensation premiums, payments to independent contractors, and payments to employees for leave covered under the Families First Coronavirus Response Act.

No. The latest guidance from the government indicates that borrows are eligible for forgiveness for payroll costs paid and payroll costs incurred, but not yet paid, during the Covered Period or Alternative Payroll Covered Period. Payroll costs are considered paid on the date of distribution of paychecks or origination of an ACH credit transaction. Payroll costs are considered incurred on the day that the employee’s pay is earned. Payroll costs incurred but not paid within the Covered Period or Alternative Payroll Covered Period must be paid by the next regular payroll date to be counted for forgiveness purposes.

The Paycheck Protection Program Flexibility Act provides that at least 60% of the covered loan amount must be used for payroll costs. If less than 60% of the loan amount is used on payroll costs, the amount of the loan that is forgiven may be reduced. The Treasury Department has indicated that at least 60% of the loan forgiveness amount must have been used for payroll costs.

You can apply for loan forgiveness through the lender that is servicing the loan. Lenders have 60 days to make a decision on loan forgiveness. The SBA has issued a loan forgiveness applications and instructions, which can be found here.

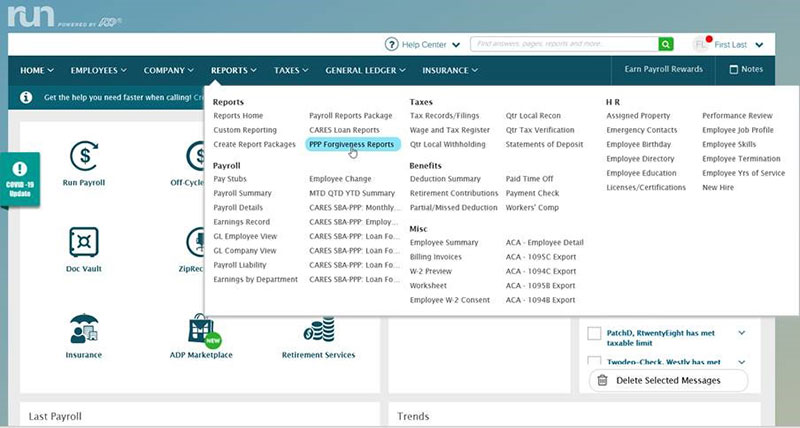

No, the ADP payroll cost and headcount reports that were developed to support PPP loan applications cannot be used for PPP loan forgiveness purposes. ADP has reports available to support clients that are navigating the forgiveness process. See below for more information about PPP loan forgiveness reports that are available.

No. Joining a PEO will not negatively impact loan forgiveness. A business that joins a PEO after receiving an SBA loan and before loan forgiveness will need to be able to produce payroll documentation for the period prior to the PEO relationship and payroll documentation from their PEO for the period following them joining the PEO relationship in order to support any request for loan forgiveness.

The Treasury Department and Small Business Administration have issued a new “3508S” version of the Loan Forgiveness Application form and Instructions, which are available here. The 3508S form significantly streamlines the loan forgiveness process for eligible borrowers.

The 3508S form is available to borrowers who obtained loans of $50,000 or less. Note, however, that borrowers that together with their affiliates received loans totaling $2 million or greater cannot use the new 3508S form. Borrowers should review 85 FR 20817 (April 15, 2020) regarding application of SBA’s affiliation rules, available here.

The 3508S form eliminates the need for borrowers to demonstrate that they maintained wage and employment levels during the applicable covered period. Instead, borrowers will need only to demonstrate that they spent the loan proceeds on covered payroll (at least 60% of the forgiveness amount) and non-payroll costs. Borrowers can download the PPP Loan Forgiveness Payroll Costs report from their ADP system to submit to their lender with the 3508S form.

For borrowers who are not eligible to use the 3508S form, the Treasury Department and Small Business Administration have also made available an “EZ” version of the Loan Forgiveness Application form and Instructions, which are available here. The EZ form contains simplified calculations and reduced reporting requirements for eligible borrowers. In order to use the EZ form, borrowers must be able to certify that at least one of three scenarios apply, as set forth on the form.

Guidance on loan forgiveness is evolving and rules may change, so check back for updates. Additionally, be sure to run your ADP PPP loan forgiveness reports as close in time as possible to when you submit your loan forgiveness application. If you’ve already received a PPP loan and are applying for forgiveness now, consider these steps to help maximize your forgivable amount:

During the applicable Covered Period following receipt of the loan...

Guidance on loan forgiveness is evolving and rules may change, so check back for updates.

Maria's Eyecare received a PPP loan of $70,000 on April 10, 2020. The company elects to use the 8-week Covered Period length to meet the criteria* for loan forgiveness. The timeline starts as soon as the company receives the loan+.

Because the company met all the criteria for loan forgiveness, the entire $70,000 loan is eligible for forgiveness.

Forgiveness Rules:

Conditions:

+ To obtain full forgiveness, loan proceeds must be spent during the Covered Period or Alternative Payroll Covered Period. To obtain full forgiveness, loan proceeds must be spent within 8 to 24 weeks immediately following disbursement of the loan, whichever is earlier. If you pay your employees on a biweekly or more frequent schedule, you may choose to use the Alternative Payroll Covered Period and begin the covered period on the first day of the first pay period following disbursement of the loan for qualifying payroll costs only.

* A loan may be fully forgiven if all the following three conditions are met:

Payroll Costs:

** Under the PPP, payroll costs generally include:

Note: The definition of payroll costs excludes employer federal taxes, workers compensation premiums, payments to independent contractors, and payments to employees for leave covered under the Families First Coronavirus Response Act.

Permitted Loan Uses:

*** PPP loans may be used for:

Staffing and Wage Levels:

**** To determine whether adequate staffing levels have been maintained, the average number of full-time equivalent employees (FTEEs) during the Covered Period or Alternative Payroll Covered Period will be compared to one of two time periods. Borrowers may either use the period from February 15 through June 30, 2019, or January 1 through February 29, 2020. Seasonal employers may compare the average FTEEs employed during the Covered Period or Alternative Payroll Covered Period to either period listed above or to any consecutive twelve-week period between May 1 through September 15, 2019. If the number of FTEEs during the Covered Period or Alternative Payroll Covered Period is lower than these earlier time periods, the amount of loan forgiveness may be reduced proportionately. However, the forgiveness amount will not be reduced by a failure to maintain staffing levels during the Covered Period or Alternative Payroll Covered Period if (a) the average FTEEs between February 15 and April 26, 2020 is lower than the FTEES as of February 15, 2020, and (b) the company restored the level of FTEEs by the end of the applicable Safe Harbor period, to be equal or higher to the FTEE levels as of February 15, 2020. The Safe Harbor period ends on December 31, 2020 for borrowers who received their PPP loan prior to August 8, 2020, and on the last day of the chosen covered period for borrowers who received their PPP loan or Second Draw PPP loan in or after December 2020. If the staffing reduction was made outside the February 15 to April 26 timeframe, the forgivable amount may still be reduced even if the staffing reduction is later reversed.

Repayment of the corresponding portion of the loan may be required if an employee’s earnings are reduced by more than 25% during the Covered Period or Alternative Payroll Covered Period compared to the period of January 1 through March 31, 2020. However, if (a) a given employee’s wage levels (annual salary level for salaried employees and hourly wages for hourly employees) between February 15 and April 26, 2020, are lower than as of February 15 and (b) you restore the wage levels by the end of the applicable Safe Harbor period, if earlier, to be same or higher than as of February 15, 2020, there will be no reduction in forgiveness based on that employee’s wage levels. The Safe Harbor period ends on December 31, 2020 for borrowers who received their PPP loan prior to August 8, 2020, and on the last day of the chosen covered period for borrowers who received their PPP loan or Second Draw PPP loan in or after December 2020. If the pay reduction was made outside the February 15 to April 26 timeframe, the forgivable amount may still be reduced even if the pay reduction is later reversed.

***** PPP loan proceeds may not be used to pay FFCRA paid sick or family leave wages for which a tax credit is allowed.

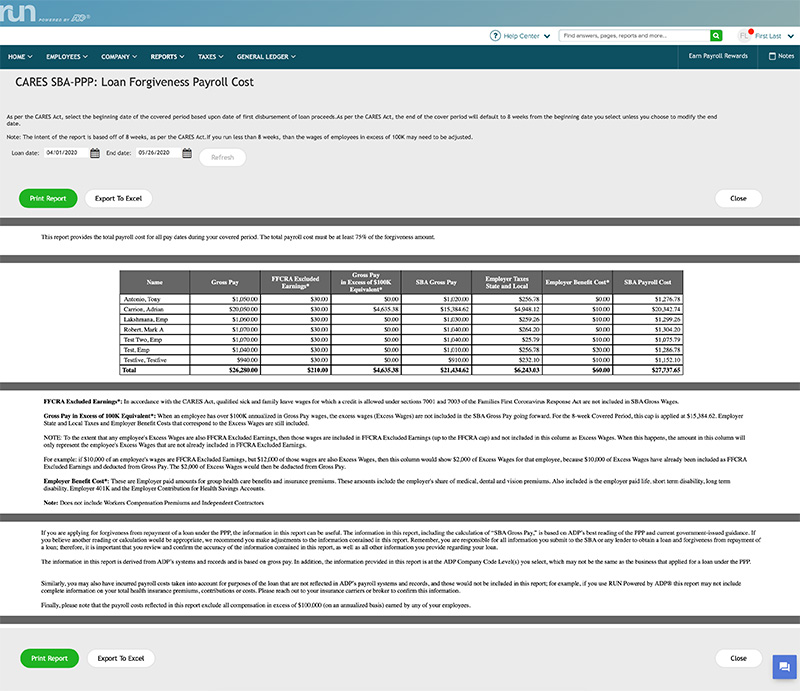

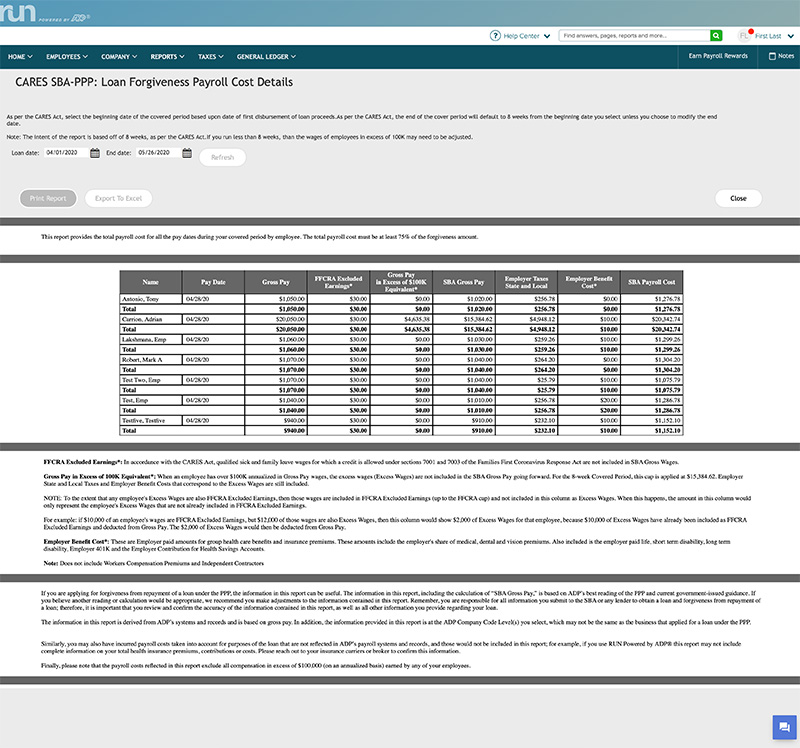

Click here for Frequently Asked Questions, including greater detail about how the reports are calculated.

For detailed information about how you will use specific data fields in these reports to fill out your PPP Loan Forgiveness Application, please see the video tutorials:

Click here for Frequently Asked Questions, including greater detail about how the reports are calculated.

For detailed information about how you will use specific data fields in these reports to fill out your PPP Loan Forgiveness Application, please see the video tutorials:

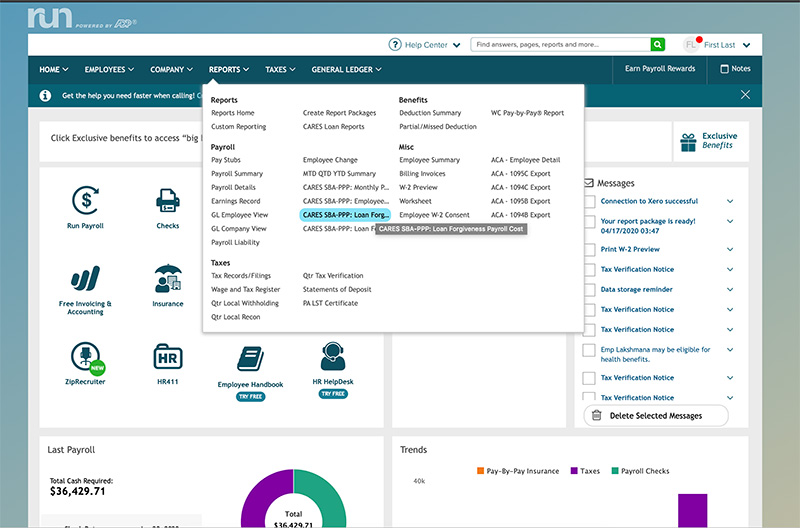

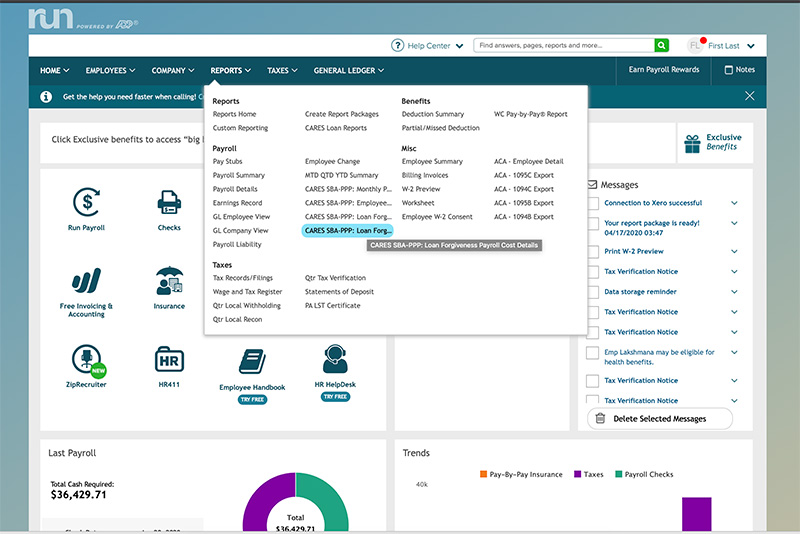

For instructions on how to run this report, please login. You’ll find the instructions on the home page.

For detailed information about how you will use specific data fields in these reports to fill out your PPP Loan Forgiveness Application, please see the video tutorials:

Click here for our Paycheck Protection Program Loan Forgiveness Estimator.

Additional Resources / FAQs

* All reports may not be available to all clients. ADP does not provide financial or legal advice. Companies should contact their financial or legal advisors or the Small Business Administration for more information regarding eligibility and their application.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}