Moving Pay from Current to Arrears? Key Considerations

Pay practices are of utmost importance to employees and employers alike, none more so than how quickly you pay your employees for time worked. Organizations may consider moving a portion or all of their employees from paying them current to arrears to standardize pay practices. The change may also reduce employee pay inquiries, rework and risk for the payroll teams.

This article outlines the considerations to evaluate when changing from current to arrears pay. It is part one of a two-part article series. Part two offers best practices for change management and communications considerations when making this change.

Pay terminology defined

Employers have two primary options in terms of how quickly they pay employees for work performed:

- Current pay: Pay employees during their pay cycle or when the pay cycle ends. Since payroll needs time to prepare the payroll, the payroll team may have to estimate the time worked and thus pay. Salaried (as opposed to hourly) employees are more "easily" paid in this method, as their pay generally doesn't change from pay period to pay period.

- Arrears pay: Pay employees for work they have already completed after the pay period ends. Arrears pay gives the payroll team time to end the pay period and prepare employee pay, associated deductions, and PTO accruals with the actual hours worked. Arrears pay minimizes back-end adjustments, particularly for hourly employees whose pay may change from pay period to pay period.

The ADP Insight article Paid In Arrears further details the pros and cons of each of these approaches.

Considerations for making a change from current to arrears pay

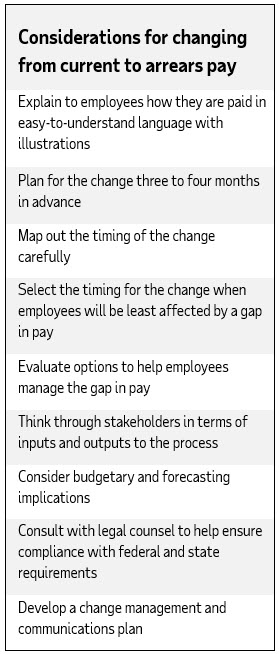

It's important to note that employees are probably unaware whether they are paid current versus arrears. Therefore, it's always a good idea to have educational materials, in easy-to-understand terms, available for employees to clearly explain how and when they are paid and what that means, specifically. In addition, before changing your pay frequency or pay timing (the time that can elapse between when wages are earned and when those wages are paid to employees) employers must first consider the legal requirements. Learn more about these requirements here.

Payroll team considerations

.

Payroll teams should carefully map out a change from current to arrears (e.g., three to four months in advance at a minimum) to allow employees plenty of time to prepare. This generally involves an initial gap in pay for employees at the time of the change. Therefore, companies should determine the timing with the least adverse impact on the employee experience. For example, while early January may initially seem a good time for the change from the employer perspective (e.g., a new year), employees will just be coming off the holidays. They may have bills to pay in January. Potential times that might be more favorable to consider making this change could be months where there are three paychecks (for those on a biweekly pay schedule) or months where employees typically are awarded bonuses (for example, the month after the quarter or fiscal year closes).

Companies changing from current to arrears pay should also think through options, if any, that their company is prepared to take to help employees manage an initial pay gap. For example, employers may offer pay cards or earned wage access to allow employees to quickly tap into their money earned as an optional benefit. They may also consider allowing employees to cash in on their PTO, awarding a bonus early, or even offering loans that employees can repay over time. However, these options do have an administrative component to keep up with. If the company provides any financial or budgeting resources through an Employee Assistance Program (EAP) or similar, consider reminding employees about these resources and how they can take advantage of them for financial planning and budgeting purposes.

The change may also impact the company's budget for the year. For example, if the company forecasts based on current pay, and then moves to arrears pay, the associated lag in pay may affect the company's budget and cash flow.

Planning for change from current to arrears pay

Payroll teams should also map out the process at a high level, clearly articulating all of the inputs and outputs to the payroll process that could be affected by the change. Teams could use a SIPOC tool (Supplier, Input, Process, Output, Customer) to visually diagram the high-level process. If the company works with an external payroll vendor(s), the vendor will likely conduct an impact analysis that assesses the effects on items such as:

- Deductions

- Any needed interim payments and manual pay interventions

- Impacts on the time collection system regarding hourly employees

- 401(k) administration, benefits administration, and impacts on other vendors and garnishment agencies

- Effects on accounting systems/general ledger/accruals

- Interfaces and calculations that should be reviewed and tested.

These changes will then be executed as a project.

Companies should consult with their legal team(s) to ensure they comply with state and federal regulations related to pay. They should be mindful of any notice requirements of unions or work councils, if applicable, and review all plans with their HR teams.

Finally, teams should also develop a change management and communications plan that clearly articulates the change, conducts stakeholder analysis, maps out communication vehicles and timing and determines any branding for the initiative.

Conclusion

By considering the considerations above, moving from current to arrears pay can be a well-planned and communicated event. It is essential to consider the employee experience and all of the other important internal and external stakeholders that could be affected. Planning for the change in advance, analyzing the effects and educating employees are critical success factors.

For more about payroll processing, including other leading practices for payroll, read "What is Payroll Processing?"