Decrease your workload while increasing your revenue opportunities. See how ADP’s solutions help you offer clients easier, better payroll & HR.

Need help? Get Support for partners.

Grow your value with a partnership powered by ADP's unmatched set of solutions for accountants.

Share in your client's success by earning revenue for referrals with our flexible partner models.

Access client reports, smart analytics, exclusive benchmark data and more, all in one place with Accountant ConnectSM.

Get the information you need fast, with secure self-service tools plus dedicated experts ready to help at a moment’s notice.

Offer easy-to-use HCM solutions for clients of all sizes – payroll, HR, time, talent, benefits, tax credits and more.

Refer clients for payroll & HR, earn rewards through our Accountant Revenue Share Incentive Program, and maintain client access with Accountant Connect.

Create year-round revenue and help strengthen CAS with payroll processing and HR management using RUN Powered by ADP® Payroll for Partners.

Already offer full-service payroll and want to know what it’s worth? Ask for a confidential valuation and strategies to transition your clients when you exit the payroll business.

Behind every business is a great accountant, but who’s behind you? That’s where Accountant Connect℠ comes in.

Did we mention it’s free?

Earn up to 75% revenue share plus ongoing residuals when you refer eligible ADP solutions to your clients for payroll, HR, benefits, tax credits & more.

Save time, streamline payroll and grow your business with the most comprehensive all-in-one service your clients can buy.

See how ADP works with accountants like you

Meet our clients

If I’m going to hand my clients over to a payroll provider, I need to know they’re going to be in good hands. The more I got to understand ADP, the more I could see how much they cared about their customers and their people.

Dawn Brolin, CPA, CPE CEO, Powerful Accounting

Meet our clients

ADP makes a great strategic partner because of all the new ways they’re working with our profession: analytics, data, insights, automation, and integrating a better human experience. ADP has the right people and the right technology to help CPAs be that value-added advisor.

Watch Testimonial See case study

Tom Hood Exec. VP Business Growth & Development, Tom Hood, CPA

Meet our clients

When leadership came together to outline what we wanted to provide our clients in the area of CAS, we considered everything from general ledger to payroll needs. RUN Powered by ADP® Payroll for Partners proved the perfect platform for us to use in our foundation of client data. It is essentially the gateway to our advisory practice.

Wade Huseth CPA, Partner, Baker Tilly

Meet our clients

Accountant Connect has really helped us to build out our CAS offering, and we now have this full seamless cloud solution for our clients.

Watch Testimonial See case study

Jennifer Brazer Founder & CEO, Complete Controller

Become indispensable to clients of all sizes with ADP’s comprehensive human capital management (HCM) solutions that offer unmatched industry-leading data, technology and service.

2022 Top New Product

2021 Top New Product

2020 Gold Stevie: Achievement in User Experience

2016-2020 Perfect 5-star Rating

2020 Top New Product

2020 Product of the Year

2020 Gold: Best New Version of the Year

2020 Gold: New Product of the Year

2020 Gold: New Product | Business-to-Business Services

2017 Top New Product

Businesses of all types and sizes turn to ADP to help them become more agile, data-driven and people-focused.

We're innovating today so our clients can find more success tomorrow.

Do more for your clients — and more for your firm. Connect with us to see how ADP can help you free up your time and enhance your service offerings.

Your privacy is assured.

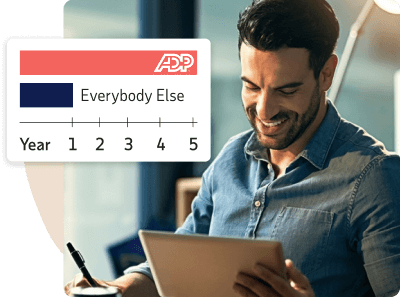

* 2023 ADP survey of 248 Accountant Connect users

†: ADP FY22 10-K